The green-tech industry is evolving at pace, shaping the future of sustainability, investment, and innovation. Staying informed about key trends, market shifts, and policy developments is crucial for businesses, investors, and sustainability professionals.

From record-breaking investment figures to novel policy developments, these 50 must-know statistics provide a full snapshot of the state of green technology in 2025.

Market Growth & Employment

- The UK’s start-up technology ecosystem is the largest in Europe, surpassing $1 trillion in valuation in 2024 and employing over 3 million people (McKinsey Sustainability, 2025).

- Over 5,200 climate tech companies operate in the UK, second only to the US globally (Tech Nation, 2022).

- The UK’s net-zero economy contributes £71 billion annually and supports 840,000 jobs (Energy & Climate Intelligence Unit, 2023).

- Employment in the UK’s green tech sector grew by 14,500 workers in 2024, reaching a total workforce of 244,500 (StartUs Insights, 2024).

- There are 9 UK climate tech unicorns (valued >$1B each) currently, with 19 future unicorns in the pipeline Climate-tech Policy Coalition, 2022).

- 17% of climate tech startups in the UK have at least one female founder, aligning with the national average (Startup Coalition, 2024).

- The global greentech market is expected to reach EUR 12 trillion by 2030 (Roland Berger, 2023).

Investment Trends

- UK climate tech startups raised £4.5 billion in 2024, a 24% increase from 2023 (Syndicate Room, 2025).

- Venture capital (VC) investment in UK climate tech reached $6.2 billion in 2023, representing 29% of all UK VC activity (dealroom.co, 2024).

- Early-stage clean tech funding grew by 158% between 2017–2021, reaching £420 million (Department for Energy Security & Net Zero, 2023).

- Octopus Group leads UK green tech fundraising with over £1.2 billion in total equity (Statista, 2024).

- Climate tech median seed round sizes grew from £260,000 in 2017 to £410,000 in 2021 (Department for Energy Security & Net Zero, 2023).

- $25 billion in new VC funds were raised by UK investors between 2021–2023 for tech deployment (dealroom.co, 2024).

- Despite global declines, UK climate tech funding fell only 4% in 2023 vs. 42% economy-wide (Startup Coalition, 2024).

- The UK government's Green Industries Growth Accelerator (GIGA), announced in 2023, established a £960 million fund to clean energy supply chains (Syndicate Room, 2025).

- Global investment in the energy transition hit $2.1 trillion in 2024, up 11% on the previous year and a new record (Bloomberg NEF, 2025).

Regional & Sectoral Insights

- Five "unicorn regions" (London, South East, East of England, South West, Scotland) collectively host startups valued over £1 billion (Startup Coalition, 2024).

- London hosts 44% of UK climate tech firms, attracting 44% of total sector investment (Startup Coalition, 2024).

- Scotland received 17% of UK climate tech grant funding in 2023, the second-highest regional share (Startup Coalition, 2024).

- Ranking third for climate tech startups, The East of England is home to Cambridge University, the joint-highest source of university spinouts (14%) (Startup Coalition, 2024).

- The energy and power sector accounts for 52% of the value of the UK’s climate tech ecosystem (Startup Coalition, 2024).

- The energy sector attracted 40% of UK clean tech investment in 2023, followed by resources & environment (19%) (Statista, 2023).

- The built environment sector represents 9% of UK climate tech firms but only 4.5% of investment secured, and 3.3% of the value (Startup Coalition, 2024).

Technology & Innovation

- The UK filed 2,700+ green tech patents in 2024, reflecting robust R&D activity (StartUs Insights, 2024).

- UK green patent filings grew 400% from 2001–2020 (GOV.UK, 2024).

- 10% of UK climate tech startups are university spinouts, led by Oxford and Cambridge (Startup Coalition, 2024).

- Digital technologies have the potential to reduce global CO2 emissions by 20% by 2030 (Digital Europe, 2021).

- Operational offshore wind capacity is on track for up to 233 GW of installed offshore wind capacity by 2030 and up to 340 GW by 2033, well short of the 2030 capacity of 494 GW that IRENA estimates is necessary to keep temperatures below 1.5°C (ERM, 2024).

- The levelised cost of electricity (LCOE) from utility-scale solar PV has decreased by 89% since 2010 (Our World in Data, 2020).

Policy & Economic Impact

- Annual UK GHG emissions fell by 53% from 1990-2023 (Statista, 2024).

- The contribution of coal to the UK energy mix has decreased by over 97% since 2013, falling to just 1% of generation in 2023 (NESO, 2024).

- COP29 reached a final agreement of a $300bn financial goal from developed countries to underdeveloped countries, far lower than economists’ estimated need of around $1 trillion per annum (McKinsey, 2024).

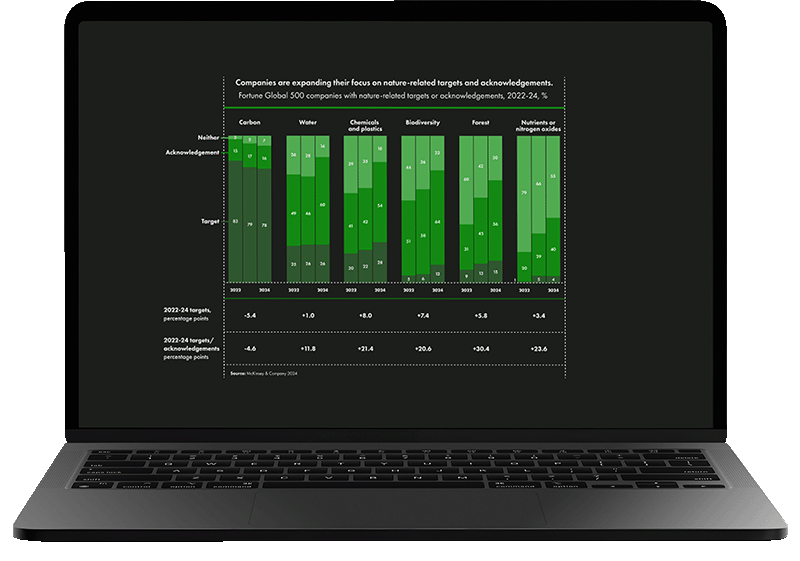

- The share of companies with three or more nature-related targets rose to 26 percent in 2024, up from 16 percent in 2022 (McKinsey, 2024).

- The UK committed £30bn in domestic green investments between 2021–2023 to meet net-zero targets (UK Green Financing Programme Allocation and Impact Report, 2023).

- The EU’s Net-Zero Industry Act aims to create 350,000 jobs via wind, solar, and battery investments (The Vienna Institute for international Economic Studies, 2024).

Challenges & Risks

- Only 7.5% of materials are circled back into the UK economy after use (The Circularity Gap Report, 2024).

- Efforts to reach net-zero globally by 2050 would require six times more mineral inputs in 2040 than today (International Energy Agency, 2021).

- AI-driven global data center electricity consumption could roughly double to 1,065 TWh by 2030 (Deloitte, 2024).

- A fully decarbonized global energy system by 2050 could cost $215 trillion, 19% more than in an economics-driven transition, where the Paris Agreement goals are missed and global warming reaches 2.6C (Bloomberg NEF, 2024).

Future Outlook

- The UK government’s Hydrogen Strategy, published in 2021, aims to achieve 5 GW of low-carbon hydrogen production capacity by 2030 (Green Hydrogen Organisation, 2022).

- The UK AI Opportunities Action Plan (2025) allocates £25 billion for data center expansion (Syndicate Room, 2025).

- The UK Emissions Trading Scheme will expand to cover the maritime sector and waste management in 2026 and 2028, respectively (GOV.UK, 2024).

- In the Net Zero Emissions by 2050 (NZE) Scenario, global production of electric cars increases six-fold by 2030; renewables account for over 60% of power generation (up from 30% today); and electricity demand increases by 25%, accounting for nearly 30% of total final consumption (up from 20% today) (International Energy Agency, 2023).

- In May 2024, Google, Meta, Microsoft, and Salesforce launched the Symbiosis Coalition, committing to 20 million metric tons of high-quality nature-based carbon removal credits by 2030 (McKinsey, 2024).

- The 2022 McKinsey Consumer Pulse Mobility Survey found 42% of respondents stating that they want their next car to be an electric vehicle (McKinsey, 2022).

- Clean hydrogen demand is projected to increase to between 125 and 585 million tonnes per annum by 2050 (McKinsey, 2024).

Global Comparisons

- The UK ranks #3 globally in tech innovation, behind the US and China, and #1 in Europe (dealroom.co, 2024).

- UK climate tech VC funding represents 40% of Europe’s total, exceeding France and Germany combined (dealroom.co, 2024).

- 99% of Uganda’s electricity generation comes from renewables, largely due to hydropower dams on the Nile River (Bloomberg NEF, 2024).

- Asia Pacific attracted the most new investment in global renewable energy during 2022, accounting for $356 billion of the sector’s $532 billion value (World Economic Forum, 2023).

As the green-tech sector continues to expand, so do the opportunities for innovation, investment, and leadership. The numbers speak for themselves - momentum is building, and businesses that embrace green technology today will shape the future of our economy and environment.